In Part I of this article, we explained how you, as a retirement plan trustee (or the administrative committee responsible for investing plan assets), can better find your way through the fiduciary forest of competing pension plan investments if you:

- Step back and get a feel for the “lay of the land” before you charge forward;

- Understand the general financial and legal goals and constraints of pension investing;

- Develop a specific written plan of action, aka, an “investment policy,” to follow and measure your progress against; and

- Hire a professional money manager, or managers, to carry out your investment policy on a day-to-day basis and to insulate you from fiduciary liability.

In this installment, we’ll equip you for the perilous journey with some lessons and guidelines for surviving in the investment jungle. We’ll talk about:

- Those you’re likely to run into along the way who may offer investment advice (or directions) for reaching your plan’s investment goal.

- The alternative modes of transportation available to you (i.e., investment vehicles).

- Basic concepts, rules, and terminology used in portfolio management theory (i.e., the law of the jungle) that may help you to make some sense of the various claims of would-be advisors and the wide variety of investment choices.

Who And What You Are Likely To Run Into Along The Way

At the end of our last episode we left our hero/plan fiduciary wandering aimlessly in the pension investment forest without a compass or a map to follow. Little does he know that he is about to cross paths with a number of helpful (and not so helpful) residents of the forest, all of whom are willing to serve as a guide to our hero . . . for a fee, of course. Who are these potential trail guides? What range of fees might they charge? There are several options by which a small or medium-sized investor, such as a pension plan trustee, can obtain investment advice and/or investment management services.

The Broker And The Traditional Brokerage Account

A broker is an agent who handles the public’s orders to buy and sell securities, commodities, or other property. For this service, the broker receives a brokerage fee, or commission, which is either an amount per transaction or a percentage of the total value of the transaction. The amount of fees you will pay in connection with a retail brokerage account depends on how much you, as fiduciary, buy and how often you buy. If, for example, you are purchasing stocks as plan investments and the broker makes recommendations for investment changes at the turnover rate of the average growth mutual fund, you will sell 100% of your stock over the course of a year. With typical retail brokerage rates, this could cost the plan as much as 4% – 5% of the money under management. Obviously, this cost can be substantially reduced by reducing the frequency of trades. Because the typical broker’s commissions are a direct function of the number of trades made by your plan account, there is a potential for “churning” to occur; that is, excessive trading in the account and without regard to the true objectives and interests of you as the client.

The Wrap Account

Wrap accounts are arrangements where a number of financial services are “wrapped” together and paid for with a single fixed fee (usually such fees are between 2% and 3% of assets under management and are billed quarterly). Unlike a traditional brokerage account, however, you are not charged a commission for the buying or selling of securities within your account. Generally, the services provided under a typical wrap arrangement include:

- Manager Search. Assisting you in searching for and selecting an appropriate investment manager, or managers, from a large universe of potential investment managers.

- Custody of Assets. This is physically holding the cash and securities comprising your account (of course, this is a service that brokerage houses routinely supply in any event).

- Management. The funds that have been placed in the custody of the brokerage house must be managed by the investment manager selected by you in accordance with your stated investment policy (see Part I for what a typical investment policy might include).

- Executing Transactions. This is the process of actually executing or carrying out the trades called for by the investment manager. The brokerage house that has arranged or set up the wrap account will get paid its share of the total wrap fee by capturing the commissions relating to transactions ordered by the professional money manager. A typical split of fees between the money manager and the brokerage house might be 1% to the investment advisor/money manager and 2% to the brokerage house.

- Monitoring Investment Manager Performance. Selected investment managers must be monitored for continuity of their investment professionals (i.e., is the team of managers you originally selected still the same?) and for their overall performance within the constraints of your investment policy.

Since most wrap arrangements are set up through brokerage houses or financial planners, the services relating to the manager search and the monitoring of the selected investment managers are provided by your local broker or financial planner. Because of the intense competition between wrap programs, it may be possible for you to establish a wrap account with a flat annual fee of 2% or less. It never hurts to ask.

An Investment Advisory Account

An alternative to a typical wrap arrangement is a direct investment advisory account. In this case, you hire an independent investment advisory firm to manage the investments with respect to all or a portion of your plan assets. A typical charge for an independent money manager is .50% to 1% of assets under management. In addition, the money manager will search out the most cost effective investment vehicles with one or more mutual fund providers and will usually negotiate an annual fund expense of approximately .20% to 1.25%, depending on the nature of the fund. Therefore, the charges for the manager’s services and related fund expense would be approximately .20% to 2.25% on a per fund basis per year.

An alternative to the typical investment advisory account is the utilization of an institutional trust arrangement that includes money management services. A number of small and mid-sized trust institutions offer specialized custodial and money management services to pension funds. Due to the way in which these arrangements are marketed and operated, many of these trust companies can offer money management services, including custodial and brokerage components, for approximately 1.5% a year. In most cases, this fee includes a certain amount of counseling and assistance by the institution’s regional sales representative.

Discount Brokerage Account

Assuming that you are either a pioneer or a survivalist interested in doing everything on your own, you do have the option of going the discount brokerage route. You can manage your plan’s money through a discount brokerage firm and the commissions will be slightly more than 1% of each transaction. Assuming you have a 100% annual turnover rate (as a result of your investment strategies), the cost of managing your money in such a fashion will be in the range of 2% to 2.6% per year. Of course, if you take to heart some of the other lessons of portfolio management theory (see below), you will reduce the number of transactions and thereby reduce your brokerage costs dramatically. If you hold a typical stock for 5 years, the cost of your discount brokerage account could be reduced to as little 0.6%.

Independent Broker/Managers

There are a growing number of so-called independent broker/managers. These are brokers who have left the big brokerage houses to set up independent offices. Some of these “independents” will agree to manage your plan’s money for fees ranging from 0.5% to 1.0%. This results in a total management cost of between 2.0% and 2.5% for a typical account with 100% turnover.

Mutual Funds

Since all mutual funds must have a manager, or a captain of the ship, you can obtain excellent money management services by investing your plan’s assets in mutual funds. The average growth stock fund has an expense rate of 1.5%. However, some funds have expenses of as little as 1.0%. These expense ratios typically do not include the cost of institutional brokerage fees that can add approximately 1% per year to these expenses. As a result, an investor in an average growth stock fund can expect costs of approximately 2.0% to 2.5% a year. Alternatively, you can search out and select an appropriate “indexed fund.” An indexed fund is usually comprised of securities that will produce a return which will replicate (or substantially replicate) a designated securities index (i.e., the S&P 500 or Dow Jones). With an index fund, it may be possible to reduce the total cost of management to less than 0.5%.

What’s Wrong With This Picture

If we can step back from the trees and survey the forest of these various arrangements for investing plan assets, we can see that they run the gamut from providing little or no advice or expertise regarding management of plan investments to a considerable amount of advice (in the case of a wrap arrangement) concerning the selection and monitoring of a professional money manager. So, you ask, what is missing? As you will recall from Part I of this article, the key to pension investing is procedural prudence. That is, you and your advisors must be able to demonstrate all of the significant steps you have taken in developing, implementing and monitoring your plan’s investment strategy. In order to do this, you must go through the process of developing an appropriate written investment policy. If you are incapable of doing this on your own, then you will need to seek the assistance of a competent advisor to help you with this process. Most of the advisors mentioned in the arrangements discussed above acknowledge the importance of completing a survey or questionnaire to determine your plan’s risk and return objectives. Although this is a good start, the completion of a risk/return questionnaire (or an investor profile) is not the same as developing a written investment policy as required by ERISA. Therefore, in evaluating these various options, and the degree to which you need more personalized assistance or help, you should ask what types of services you will receive in connection with the development of your plan’s written investment policy. If the person you are dealing with has never heard of ERISA or does not seem to understand the importance of a written investment policy, they probably have no credible experience dealing with pension plans.

In order to sort out and differentiate between potential investment advisors and counselors who understand the special needs of ERISA pension plans, as opposed to the investment needs of an individual investor (with respect to his own money), you need to be familiar with the various asset classes as appropriate plan investments as well as several basic principles of portfolio management theory.

The Alternative Modes Of Transportation Available To You

Getting from point A to point B can be done in any number of ways. There are a wide variety of investment vehicle alternatives available to a plan fiduciary. The universe of investment alternatives is generally broken down into “asset classes.” It is important for a fiduciary to understand the risks of various classes of investments and how the various classes differ. In comparing potential investments in various asset classes, you and your financial advisors should discuss the differing levels of financial, interest rate, political and social change risks in connection with each class. Furthermore, certain classes of investments have distinct (and often troublesome) characteristics in terms of marketability, liquidity, stability in value and the potential for growth. In general, you should avoid plan investments that have no ready market value. The following is a partial list of several commonly considered classes of investments with a thumbnail sketch of their basic characteristics:

Common Stock

Common stock generally refers to an ownership or equity interest in the earnings or assets of a corporation. Stock ownership can be rewarded either by the payment of dividends or the enhanced value of the stock itself. Common stock (if traded on a national exchange) is relatively easy to purchase, to value and to sell. Values are published daily in most newspapers. Since the value of publicly traded stock is established in the market place, stock prices are subject to fluctuation even if the company itself has not undergone significant change. Therefore, there is a definite risk of negative price fluctuation in common stock holdings. As a class, however, common stock has been shown to permit investors to achieve a historical rate of return greater than inflation.

Bonds, Notes, and Debentures

A bond is a debt instrument under which the issuer agrees to repay the principal amount at a future date and to pay interest at a stipulated rate during the life of the bond. Bonds can be either secured (by pledge of specific property; e.g., a mortgage bond) or unsecured (in the case of debentures or notes) which merely represent a contractual promise to pay both interest and principal. Although the pledge of property to secure a bond may enhance its value, the most important consideration regarding the quality of the bond is the overall financial strength of the issuer. The more solid the issuer, the less chance of default and the lower the rate of interest the issuer must pay in order to borrow. In general, U.S. Government, Government-Guaranteed and Government Agency debt are considered to be of the highest quality. The quality of commercial and industrial debt depends on the financial and operational strength of the issuer and is subject to a wide variety of ratings provided by various investment advisories. In general, publicly issued bonds are relatively marketable. Prices can do fluctuate however. Changes in the price of bonds can be due to either a perceived change in the financial strength of the issuer (in its ability to repay) or, more likely, due to the change in the general level of interest rates. As interest rates rise, the value of outstanding bonds generally decline.

Money Market Instruments

At any given time, a plan or a fund’s investment manager may want to hold some money in reserve or “in cash.” Even though such money is not in either stocks or bonds, it is still possible to earn some rate of return utilizing money market instruments, which carry little risk. Examples of typical money market instruments include: U.S. Treasury bills; bank repurchase agreements; bank short-term investment funds; negotiable certificates of deposit; and money market mutual funds.

Mortgages and Real Estate

Mortgages are loans (or interests in a pool of loans) secured by real property. Mortgages can be either insured by a U.S. Government agency, such as FHA insured or VA insured, or uninsured (perhaps with the exception of private mortgage concerns). An investment in “real estate” generally refers to a direct ownership of real property (e.g., a shopping center, office building, or industrial building). Many investors feel that investments in mortgages and real estate can provide an attractive yield relative to risk, a means of diversifying a portfolio and a partial hedge against inflation. On the other hand, the often cited disadvantages of mortgage and real estate investments include reduced marketability, need for special expertise in evaluating and monitoring property investments, the potential need to reinvest cash flow resulting from mortgage payment or prepayments and the unique complexity of financing and handling real property investments.

Private Placements Including Non-Publicly Traded Limited Partnerships

A substantial number of small pension plans, particularly those controlled by doctors, lawyers and other professionals, have invested in private placements. Private placements are limited offerings (i.e., sales) of securities. That is, they are not offered to the general public, but only to qualified investors. They typically have been offerings of limited partnership interests. One advantage of private placements is that they generally involve less expense than a public offering; therefore, a potential higher yield to an investor. Since such investments are not publicly offered and have not been registered with the Securities and Exchange Commission, however, they often involve considerable risk and are often almost totally illiquid. Another important consideration in investing in private placements is the difficulty in obtaining a fair market value for purposes of reporting on retirement plan financial statements and returns. Finally, if you have too large a percentage of this type of asset in your plan, you may become subject to special audit or bonding rules.

Insurance Company Alternatives

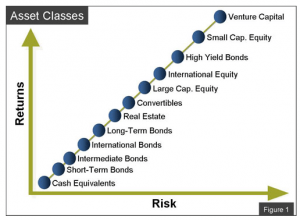

Since insurance companies themselves are responsible for investing huge amounts of money, such companies are constantly involved in direct investments on behalf of pension clients in all of the various investment classes mentioned above (and others). One of the primary advantages of investing through an insurance company is based on the fact that insurance companies are capable of pooling tremendous amounts of capital for investment in a wide variety of asset classes and economic sectors within a class. Therefore, an investment through an insurance company can benefit from substantial “economies of scale.” Although certain pension clients can establish “separate accounts” in order to better target the investments made on their behalf by the insurance company, most smaller pension funds are invested in the insurance company’s “general account” which is a broad collection usually consisting of mortgages, direct placements and other asset classes. Generally, the operation of such general account investments is such that the rate of return credited on money invested with the insurance company may be higher than the rate of investment actually earned on such assets. As a result, there is usually a corresponding “market to market” adjustment if the plan withdraws money, and certain restrictions or penalties on the withdrawal of money other than over an extended period of time (e.g., 10 years). Often times, life insurance companies will issue “guaranteed” interest or guaranteed investment contracts (sometimes referred to as GICS) under which they guarantee the principal and minimum rate of interest. Figure 1 provides a good indication of the relative characteristics, in terms of risk and return, of various asset classes.

The Basics Of Portfolio Management Theory (Or “It’s The Law Of The Jungle”)

In developing a written investment policy for your plan and selecting an appropriate investment manager, or mangers, to be familiar with a few fundamentals of portfolio management so that your career as a plan fiduciary will not end up nasty, brutish and short:

Risk and Return are Related

Generally speaking, the greater the level of risk that the plan’s fiduciary is willing to assume, the greater the potential return. For investors, risk is defined as the probability or likelihood of not achieving the plan’s investment goals within a set period of time. Often, potential investment risk is measured in terms of the degree to which actual returns may vary from historical, median returns. These variances can be expressed in terms of “standard deviations” (i.e., the statistical likelihood that actual returns will fall within a given range of returns or group around the expected return) or “Betas” which are a statistical estimate of the average change in your portfolio’s rate of return corresponding to a 1% change in the market as a whole. If you plan to obtain a long-term return in excess of inflation, you probably will need to accept some risk by investing in growth equities (and not simply rely on cash and/or fixed income securities).

Asset Allocation is the Single Greatest Determinant of Portfolio Performance

A number of studies have concluded that the asset allocation decision, or the process of optimizing the mixture of various types of assets comprising a portfolio, can on a long-term basis account for as much as 92% of the portfolio’s overall performance. By comparison, these studies conclude that 2% of overall performance may be attributed to timing decisions, 3% to security selection (e.g., the choice of one high-tech stock over another) and 3% to luck. If you assume that the results of such studies are even remotely accurate, you must be wondering why so much effort and money is expended on investment manager searches rather than on the asset allocation decision and the related decisions of when and how to “rebalance” the asset allocation.

Time is the Investor’s Greatest Ally

History has consistently demonstrated that the longer a given portfolio can remain invested, the more aggressively the portfolio can be diversified without increasing the assumed risk of the portfolio. This is because the variance of returns (standard deviation) tends to get smaller over longer periods of investment. Put another way, the degree of variance observed in a typical equity portfolio over a five-year period will be less than one-half the variance of the same portfolio over a one-year period.

Seek the “Efficient Frontier”

Based on the ground-breaking work of Dr. Harry Markowitz, the father of modern portfolio theory, the so-called “efficient frontier” is the result of complex computer modeling which explains how, in most cases, a portfolio can be optimized. The efficient frontier demonstrates that for any given expected rate of return, an ideal mix of asset classes can be formulated that will produce the expected rate of return with the least amount of volatility or risk. It also con- firms that for any level of assumed risk, a higher expected return may be achieved by combining various asset classes rather than by investing in a single asset class. This type of analysis can be invaluable in the development of your plan’s investment policy and asset allocation strategy.

Hold Reasonable and Realistic Expectations

As mentioned earlier, the relationship between risk and return dictates that the higher the expected rate of return, the greater the associated investment risk. If you, as a plan fiduciary, set unrealistic or unreasonable performance expectations for your plan’s portfolio (that is, you are striving for unusually high returns), you will expose the plan, and yourself, to unnecessary loss (and possible liability). While it is to be expected that a fiduciary will seek an overall return that at the very least will yield real growth above and beyond the rate of inflation, it may no longer be realistic for a fiduciary to be “chasing” the extraordinary double-digit returns of the bull market of the 1980s and the late 1990s.

What To Do?

First of all . . . take heart! As demonstrated by this relatively simple two-part article, the process of prudently investing the assets of an ERISA plan need not be overwhelming or overly burdensome. In Part I, we described a four-step process for assessing your situation, under- standing your duties and obligations, developing a plan of action and securing professional help to develop and implement your plan. In Part II, we have continued to equip you with some of the information you will need to help you select the right trail guide and the correct mode(s) of transportation for making your journey. We have also taught you a few rules of survival in the investment jungle to help you get your bearings and avoid taking too risky a path.