Second in a Series

Key Takeaways

- Businesses under common ownership may have to be treated as a single employer for employee benefit plan purposes.

- Controlled group rules can apply even when the businesses are in different industries, have separate operations, or do not share employees.

- There are three main types of controlled groups: parent-subsidiary, brother-sister, and combined controlled groups.

- Ownership attribution rules can cause one person to be treated as owning interests held by family members, entities, trusts, estates, or option holders.

- Separate legal entities and separate EINs do not prevent controlled group treatment.

Controlled group issues often arise in situations that look ordinary from a business perspective: an owner has more than one company, a family owns interests across multiple entities, a holding company owns several operating businesses, or a business is restructured over time.

For employee benefit plan purposes, those separate entities may not be separate at all. If the controlled group rules apply, the employees of all controlled group members may have to be treated as employed by one employer for many benefit plan purposes.

The part that catches many owners and advisors off guard is that the businesses do not have to be operationally connected. They may have different employees, different locations, different customers, and different lines of business. The controlled group analysis is driven primarily by ownership.

Back to SMALLCO and SMALL Vineyards

In the first article in this series, the owners of SMALLCO, their accountant, and their retirement plan third party administrator discovered that SMALLCO’s retirement plan may have had a problem because the owners also owned SMALL Vineyards.

The businesses were very different. One was a manufacturing business. The other was a winery.

But for employee benefit plan purposes, that difference may not matter.

If SMALLCO and SMALL Vineyards are members of a controlled group, certain Internal Revenue Code and ERISA rules treat the employees of both businesses as employed by a single employer for many employee benefit plan purposes.

What Is a Controlled Group?

There are three basic types of controlled groups:

- Parent-subsidiary controlled groups

- Brother-sister controlled groups

- Combined controlled groups

Each type is based on ownership.

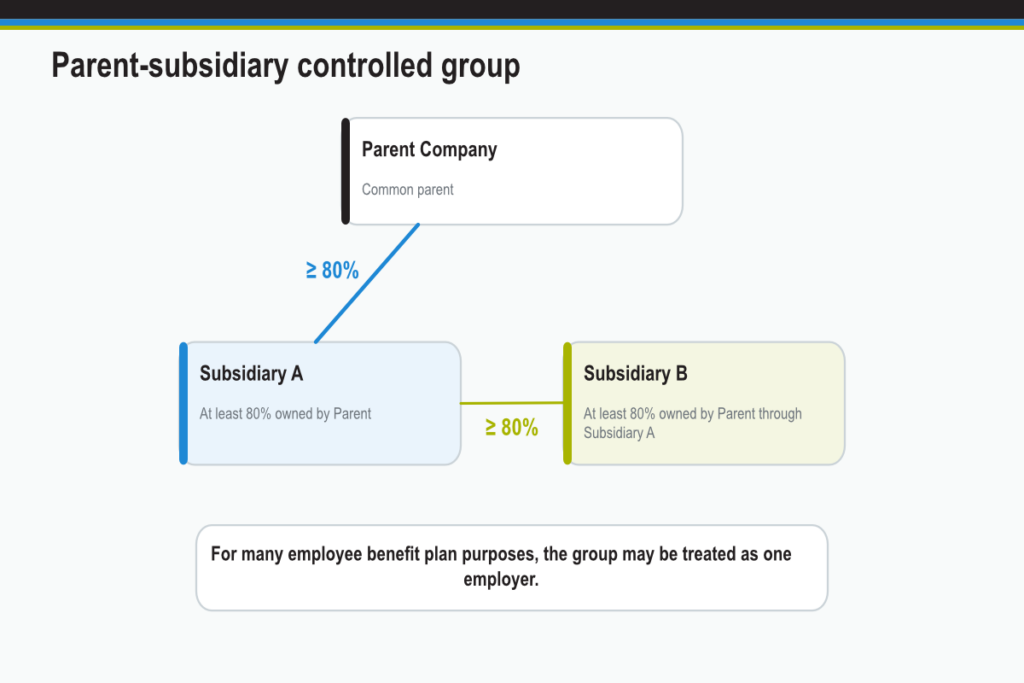

Parent-Subsidiary Controlled Group

The simplest parent-subsidiary controlled group exists when one business owns at least 80% of another business.

The ownership may be direct or indirect. A parent-subsidiary controlled group can also include a chain of businesses if the ownership requirements are met through multiple entities.

For example, if Parent Company owns at least 80% of Subsidiary A, and Subsidiary A owns at least 80% of Subsidiary B, the companies may be part of a parent-subsidiary controlled group.

Brother-Sister Controlled Group

The simplest brother-sister controlled group exists when one individual owns at least 80% of two or more businesses.

When multiple owners are involved, the analysis becomes more complicated.

In general, a brother-sister controlled group exists when five or fewer owners who are individuals, estates, or trusts collectively own:

- At least 80% of each business; and

- More than 50% of each business, counting each owner’s interest only to the extent that the ownership is identical with respect to each business.

An owner’s interest is not counted unless that person owns an interest in each business being analyzed.

Combined Controlled Group

A combined controlled group consists of three or more businesses where:

- Each business is a member of either a parent-subsidiary controlled group or a brother-sister controlled group; and

- At least one business is both the common parent of a parent-subsidiary controlled group and a member of a brother-sister controlled group.

Combined controlled groups are less intuitive, but they often arise in more complex ownership structures.

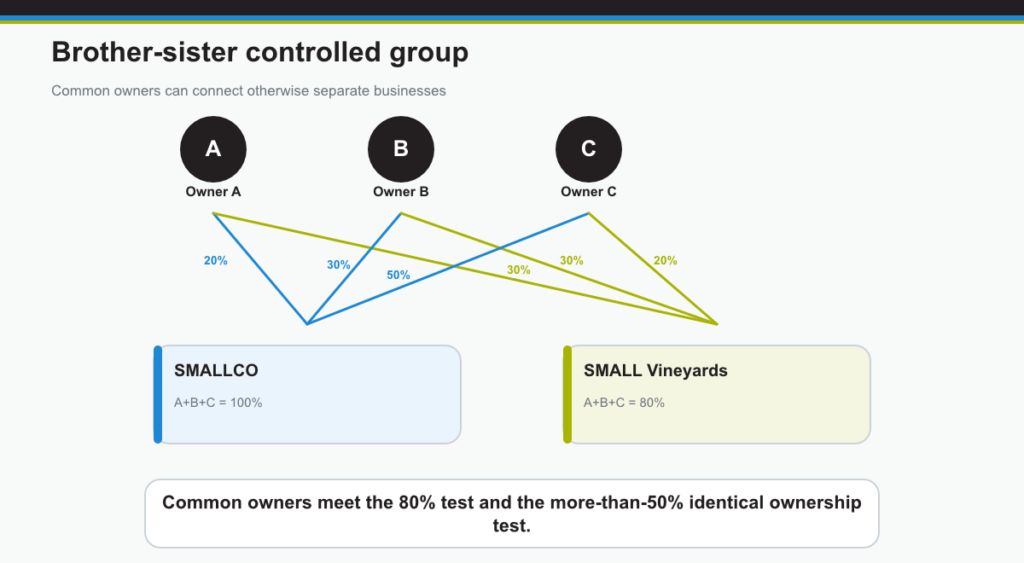

How SMALLCO and SMALL Vineyards Were Caught

Assume the ownership of SMALLCO and SMALL Vineyards looks like this:

| Owner | SMALLCO | SMALL Vineyards | Identical Interests |

| A | 20% | 30% | 20% |

| B | 30% | 30% | 30% |

| C | 50% | 20% | 20% |

| D | 0% | 20% | 0% |

A, B, and C collectively own at least 80% of each business.

They also own more than 50% of each business when counting only their identical ownership interests.

As a result, SMALLCO and SMALL Vineyards are a brother-sister controlled group.

D’s 20% ownership of SMALL Vineyards is not counted because D does not own any interest in SMALLCO.

If the ownership changed so that A owned only 25% of SMALL Vineyards and D owned 25%, no controlled group would exist under this example because A, B, and C would collectively own only 75% of SMALL Vineyards.

The Businesses Do Not Have to Be Related Operationally

One of the most important points about the controlled group rules is that the businesses do not have to be operationally related.

It generally does not matter whether the businesses:

- Operate in different industries

- Have different locations

- Have different employees

- Do not share customers

- Do not share vendors

- Have no business dealings with each other

- Were not structured to avoid employee benefit plan rules

The key issue is ownership.

For example, if two U.S. corporations are wholly owned by a foreign parent corporation, the two U.S. corporations may be members of a controlled group even if they operate in different industries and have no contact with each other.

What About Separate Lines of Business?

The separate line of business rules, often referred to as the “SLOB” rules, may provide relief in limited circumstances.

Under Code section 414(r), certain employers that would otherwise be aggregated under the controlled group rules may be treated separately for specific purposes, including:

- Retirement plan coverage and discrimination testing

- Dependent care assistance program nondiscrimination testing

The SLOB rules are technical and limited. Generally, each separate line of business must have at least 50 employees and must satisfy other requirements showing operational independence.

The SLOB rules are not a general exception to the controlled group rules. They should be analyzed carefully before relying on them.

Ownership Attribution Rules

The controlled group rules do not look only at ownership held directly.

In many cases, one person or entity may be treated as owning interests held by someone else. These are called ownership attribution rules.

Attribution can change the controlled group analysis dramatically.

Options

Ownership of an option is generally treated as ownership of the underlying interest.

Partnerships

A partner who owns 5% or more of a partnership may be treated as owning a proportionate share of the partnership’s interests in other businesses.

Estates and Trusts

A beneficiary who owns 5% or more of an estate or trust may be treated as owning a proportionate share of the estate’s or trust’s business interests.

Corporations

A shareholder who owns 5% or more of a corporation may be treated as owning a proportionate share of the corporation’s interests in other businesses.

Minor Children

A parent may be treated as owning interests owned by the parent’s minor children, and each minor child may be treated as owning the interests owned by the child’s parents.

For years beginning after December 31, 2023, the minor child attribution rules were modified in certain ways. For example, if a minor child is treated as owning two different businesses because of attribution from each parent, that attribution alone will not cause the businesses to be members of the same controlled group, absent spousal attribution.

In addition, for years beginning after December 31, 2023, ownership is not attributed to a spouse solely through the combined application of the option attribution rule and the minor child attribution rules.

Adult Children, Parents, and Grandparents

An individual who owns more than 50% of a business may be treated as owning interests held by the individual’s parents, grandparents, grandchildren, and adult children who have reached age 21.

Spouse

An individual is generally treated as owning the interests owned by the individual’s spouse.

There is an exception, but it is narrow. The non-owner spouse generally will not be treated as owning the owner spouse’s business interest for a taxable year if all of the following are satisfied:

- The non-owner spouse does not directly own any interest in the business during the year.

- The non-owner spouse is not a director, fiduciary, or employee of the business and does not participate in management during the year.

- No more than 50% of the business’s gross income for the year is derived from royalties, rents, dividends, interest, and annuities.

- The owner spouse’s interest is not subject to certain restrictions that run in favor of the non-owner spouse or the non-owner spouse’s minor children.

Community property laws can complicate this analysis for years beginning before January 1, 2024. For years beginning after December 31, 2023, community property laws are disregarded for purposes of determining ownership under these rules.

Are Any Interests Excluded?

Some interests are treated as not outstanding for purposes of the controlled group rules.

These include:

- Treasury stock

- Nonvoting stock that is limited and preferred as to dividends

Additional exclusions may apply in parent-subsidiary or brother-sister controlled group analyses.

For example, if a parent business owns at least 50% of a subsidiary, certain subsidiary interests may be excluded when determining whether the parent and subsidiary are members of a parent-subsidiary controlled group. These may include certain interests held by deferred compensation trusts, certain owners or employees, or certain tax-exempt organizations.

Similarly, in a brother-sister controlled group analysis, certain interests may be excluded if five or fewer persons own at least 50% of a business. These may include certain interests held by a qualified retirement plan, certain restricted employee ownership interests, or certain tax-exempt organizations.

These exclusions are technical and fact-specific. They should not be assumed without a careful review.

Practical Warning Signs

A controlled group analysis should be considered when:

- The same person or family owns multiple businesses

- A holding company owns operating companies

- One entity owns 80% or more of another entity

- Several people own interests in the same group of companies

- Spouses, children, trusts, estates, partnerships, or corporations own interests

- A business is buying, selling, spinning off, or restructuring entities

- A retirement plan covers employees of only one entity in a larger ownership structure

What to Do

If there is any doubt about whether a controlled group exists, the ownership structure should be reviewed before employee benefit plan decisions are made.

Business owners and advisors should gather:

- A list of all related and commonly owned entities

- Direct and indirect ownership percentages

- Family ownership information

- Trust, estate, partnership, and corporate ownership information

- Option agreements or other rights to acquire ownership

- Employee benefit plan information for each entity

The controlled group rules are ownership-driven and can apply even when the businesses appear unrelated from an operational standpoint.

That is why these questions should be asked early, not after plan testing, a transaction, or an employee claim has already exposed the issue.

Read the Full Series

This article is part of a series on employee aggregation rules for benefit plans.